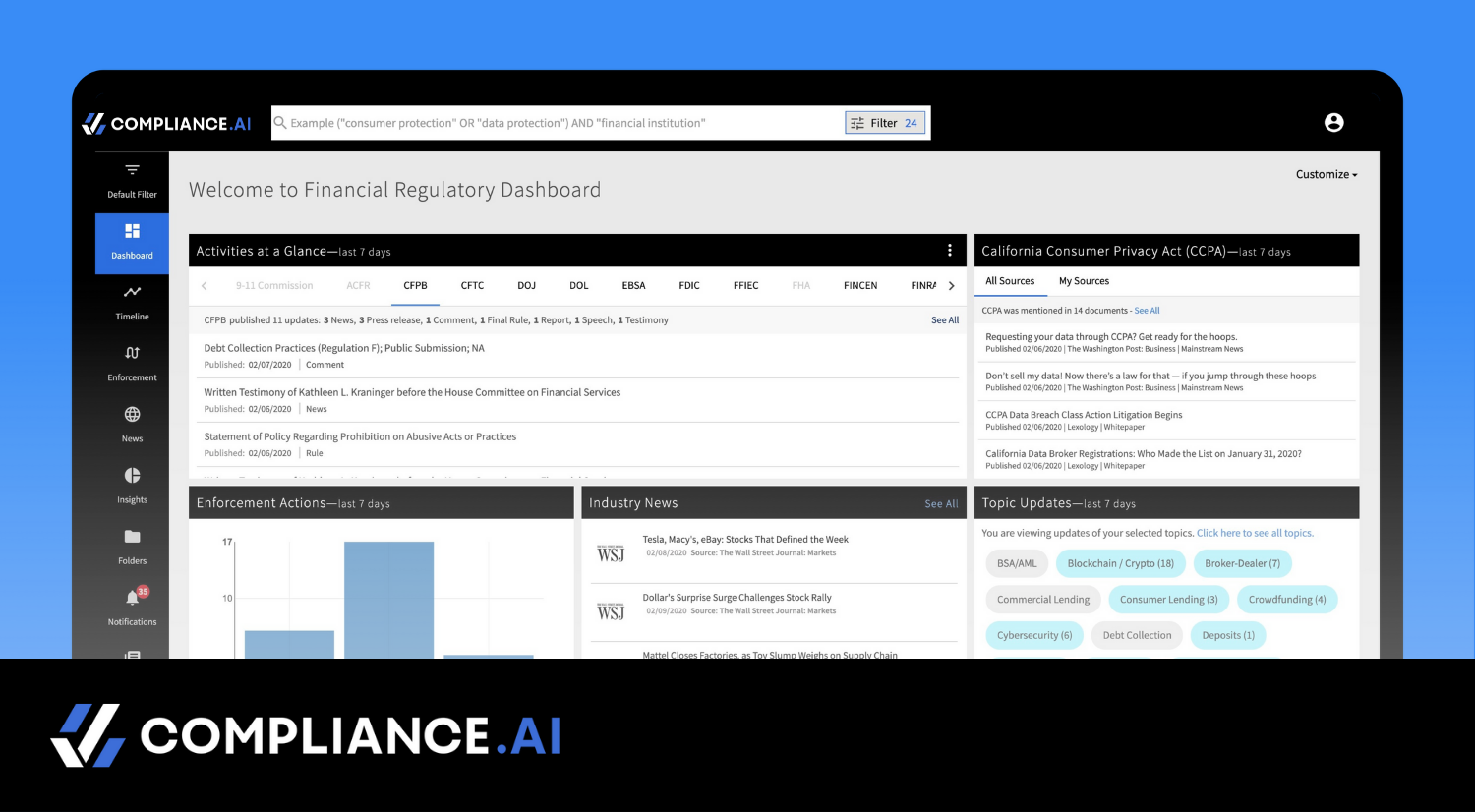

How Do You Keep Up with New Obligations?

The next part of our “Day in the Life of a Compliance Officer” blog series is going to take a deep dive on one of the most complex and dynamic pieces of the Compliance Management System, staying current with new rules and regulations. The Change Management Program outlines how a bank identifies, evaluates, implements and validates changes related to regulations or updates coming from an agency. These changes can come from any number of sources from the state or federal level, and even from supervisory agencies. The banking industry is one of the most heavily regulated industries, and the process has only become more cumbersome after the Dodd-Frank Act in 2010. The Dodd-Frank Act was the government’s response to the financial housing market collapse in 2008 and outlined a variety of mandated reform efforts and consumer protection initiatives. The most significant outcome was the creation of the Consumer Financial Protection Bureau (CFPB) to oversee the current regulations and develop and implement the reform outlined in the Dodd-Frank Act. Other federal agencies that maintain oversight of the financial services industry include: the Department of Justice (DOJ), the Financial Industry Regulatory Agency (FINRA), the Treasury (TREAS), the Federal Financial Institutions Examination Council (FFIEC), and many more. Trying to sift through all the news and updates from the bureaus and agencies can be time-consuming and challenging to filter through the irrelevant noise coming from mainstream news and unaccredited sources. We will zoom in on this aspect of information collection in Part Three of this blog series.

Source: CartoonStock.com

Source: CartoonStock.com