Following the Money

That’s where RegTech can help.

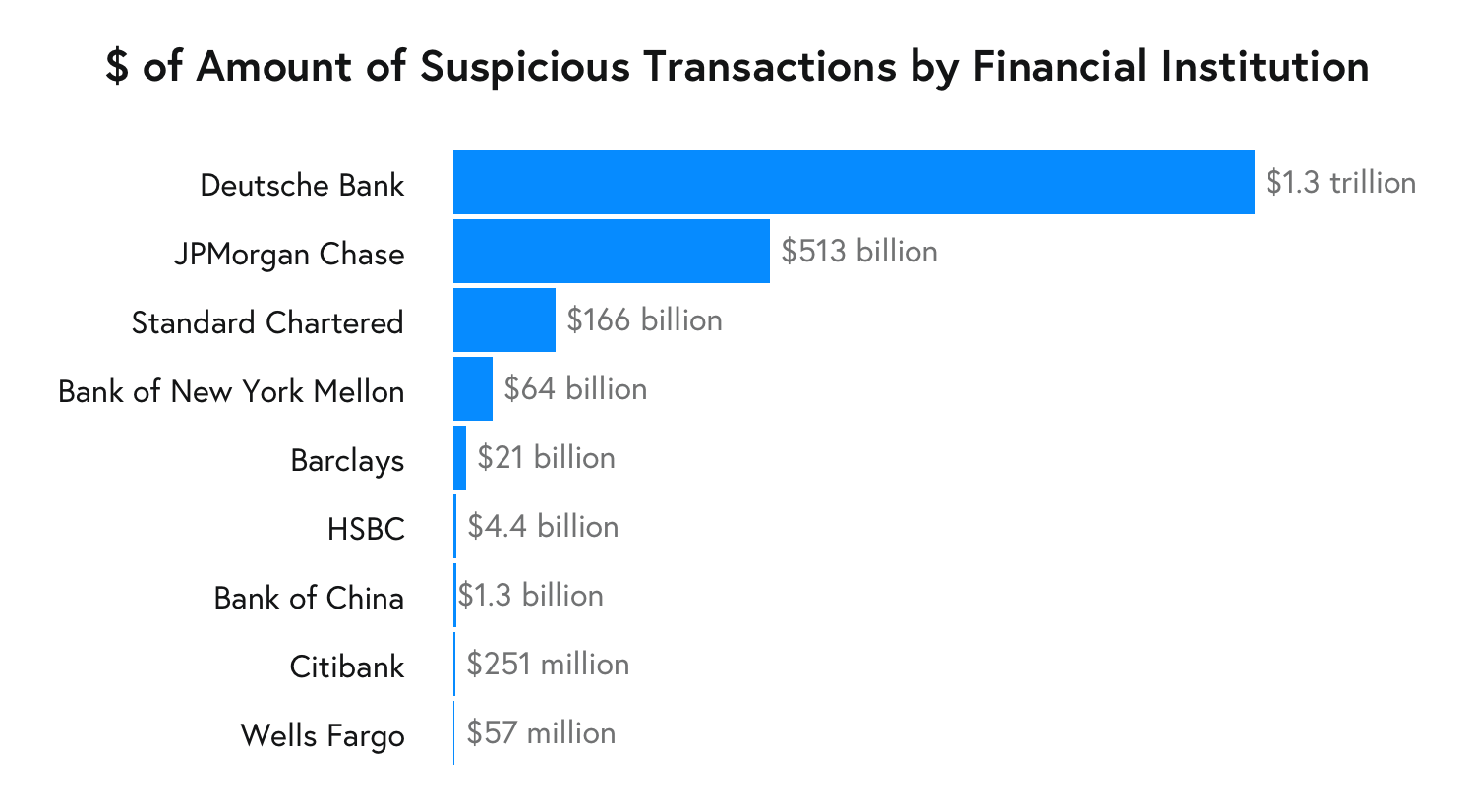

According to the ICIJ report, banks and credit unions – online and off – have significantly limited abilities to track suspicious payments. In fact, they were only able to track a “miniscule” amount of SARs alerts, with even lower successful outcomes in rooting out financial fraud. With results like that, criminals will only grow more emboldened in pushing through financial payment firewalls to their advantage.

RegTech tools can thwart those efforts, and it all begins with a robust focus on getting, reviewing and disseminating data that can make key distinctions on suspicious payments.

This from a recent report on financial fraud from Accenture:

Data analytics – the lifeblood of regulations. To meet regulators’ prospects, banks essentially store, access and process data on a measure never previously predicted. Data sets must be deep, accurate, and their contents should be able to be cross-examined, viewed and operated with much more flexibility than earlier, with different potentials and for different purposes.

RegTech provides not just solutions to report or monitor for banks to remain compliant but also provides solutions constructed around the data.

On the one hand, advanced technologies make a significant positive impact on alternative data sources, enabling better decision-making and rigorous research and processing of unstructured data for intelligent management. On the other hand, advanced technologies are interactive, adaptive, collaborative and intelligent, and thereby reducing the complexity, accelerating time to analysis and adding value to company financial data tracking efforts.

Getting Off the “Suspicious Payments” List

As the old business saying goes, preventing risks is preferable to dealing with risks after it’s too late.

Since, banks and financial institutions get and track thousands of financial fraud alerts and suspicious notification alerts on a daily basis, the trick for financial institutions is to figure out which suspicious payments need immediate follow-up, as they represent the biggest risk to banks and financial services companies.

With RegTech tools like anti-money laundering (AML) protection via “smart” applications, anti-transaction fraud detection software that operate on a single-risk platform, and communication tracking via machine learning and behavioral data software, financial institutions can leverage RegTech to minimize money lost due to suspicious payments that prove to be suspicious for a good reason.

In the process, banks and other industry firms that handle a substantial amount of financial transactions (digitally and otherwise) and keep their names off those ubiquitous lists of financial services companies that lose large sums of money due to suspicious payment activity.

Automatically monitor regulatory updates to map to your internal policies, procedures and controls. Learn More

Automatically monitor regulatory updates to map to your internal policies, procedures and controls. Learn More