How will the Bank Secrecy Act affect Cryptocurrency Regulation?

If you haven’t heard of cryptocurrency lately, then you might be hiding under a rock because the new form of virtual currency has taken the world by storm. There are a multitude of different cryptocurrencies out there but the most talked about one is Bitcoin. At the beginning of 2017 Bitcoin was selling for around $1,000 per coin and by the end of 2017, we saw it hovering around the $18,000 mark before falling sharply to ~$14,000. While price volatility continues. the growth has fueled a firestorm of eager investors, and many alternative cryptocurrencies such as Ripple and Ethereum have emerged with great success. The slow start of cryptocurrencies has been due to a healthy speculation as to whether consumers and businesses would latch on to the new idea of non-government backed virtual currency. As of now, it seems the public and a growing group of businesses are starting to warm up to the concept.

As more companies climb on the cryptocurrency bandwagon and begin to incorporate virtual currency into their business models, the validity of this new method of payment will start to become a prominent staple in the financial landscape worldwide. It would seem that at least for now cryptocurrencies, especially Bitcoin, are here to stay and will continue to grow in popularity. So now it’s time for people to understand how it works and how it fits into the current regulatory framework.

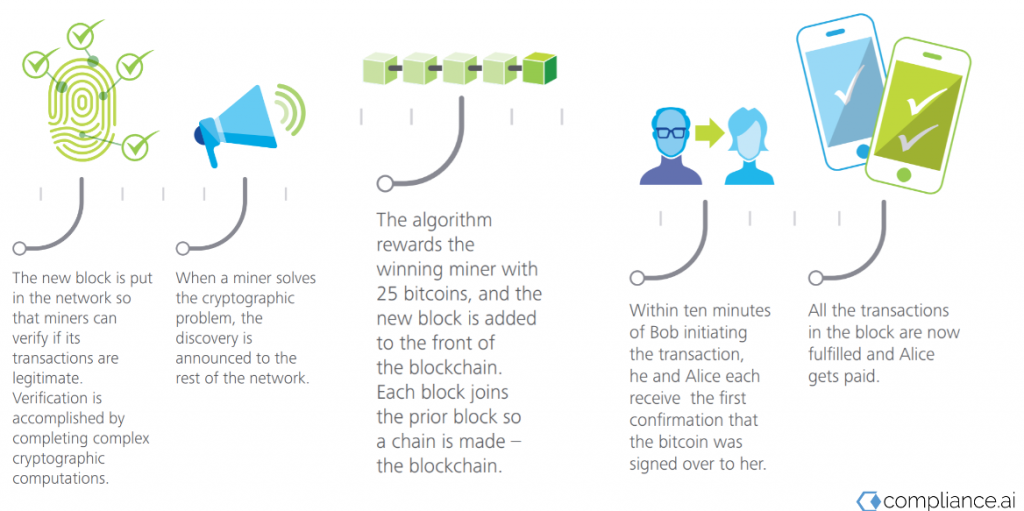

Many cryptocurrencies operate on blockchain technology which is the computer program used to process the transactions. The Harvard Business Review describes it as “an open, distributed ledger that can record transactions between two parties efficiently and in a verifiable and permanent way.”At any given time a multitude of transactions occur in the network, all pending transactions are organized in a block for miners to verify the transactions legitimacy. When the miner solves the cryptographic puzzle, the discovery is announced to the rest of the network. The algorithm then rewards the winning miner with a Bitcoin, and the new block is added to the front of the blockchain.

Source: Deloitte

A federal law, the Bank Secrecy Act (BSA), mandates that “financial institutions” must collect and retain information about their customers and their identities and share that information with the Financial Crimes Enforcement Network (FinCEN), a bureau within the Department of Treasury. Cryptocurrency raises the important question, when do business dealings with this new form of currency fit the definition of “financial institution” and become obligated to comply with BSA regulation?

In 2013, FinCEN published official guidance on the “Application of FinCEN’s Regulations to Persons Administering, Exchanging, or Using Virtual Currencies.” (Fin-2013-G001, 2013) The guidance defines “Convertible Virtual Currency,” as any virtual currency, or “medium of exchange,” that either has an equivalent value in real currency or acts as a substitute for real currency. FinCEN created this term with broad and specific intent. BSA regulates “financial institutions” with various subcategories and grants the power to craft new or more specific definitions through notice and comment rulemaking. The subcategories of “financial institutions” are focused on what activities that person and/or business performs (e.g., money transmission, foreign exchange, banking, etc.), and not focused on which technologies are used to perform those activities. The majority of these activities are defined in regards to exchanging, storing, or otherwise dealing with “currency.”

Currency is defined in BSA as “the coin and paper money of the United States or any other country.” So no activity using private currency or cryptocurrency like Bitcoin would fit within the defined activities specifying “currency” as the medium for activity.

Cryptocurrency within the current Regulatory Landscape

The “money transmitter” subcategory of “financial institution,” has a broader definition extending to money transmission involving “currency…or other value that substitutes for currency.” The newly defined “convertible virtual currency” falls into that category. Rather than crafting a newly regulated activity or technology-based regulation, FinCEN simply clarified why activities performed using Bitcoin or any other currency substitute may fit within the existing definition of “money transmitters.” This falls into the even broader category of “money service business” (MSB), and in turn, is one of the several sub-categories of “financial institution.” Because of this nesting game of word definitions in the FinCEN guidance, a virtual currency business could be classified as a “money transmitter.”

The guidance also creates and defines three categories of persons: administrators, exchangers, and users and explains in detail why only administrators and exchangers qualify as “money transmitters” and therefore must comply with BSA.

An “exchanger” is a person engaged as a business in the exchange of virtual currency for real currency, funds, or other virtual currency. An “exchanger” that accepts and transmits a convertible virtual currency or buys or sells convertible virtual currency for any reason is a money transmitter under FinCEN’s regulations. The definition does not include individuals buying or selling Bitcoin as a personal investment or for other personal purposes. “Accepts and transmits” means you take Bitcoin from one customer and send it to another person or persons on their behalf. You have to do both, accept and transmit, so if you are only accepting Bitcoin from someone or only sending Bitcoin to someone (possibly in return for a good or service), then you are not a money transmitter. You are a money transmitter if you are an exchanger who buys and sells…for any reason, such as a brokerage or exchange service for customers. If classified as an “exchanger” the business must register with FinCEN as an MSB, have a risk-based know-your-customer (KYC) and anti-money-laundering (AML) program, and file suspicious activity (SARs). The recent upswing in new KYC requirements for new and existing cryptocurrency wallet owners internationally suggests that such standardization could be crucial for ensuring the proper functioning of the growing future cryptocurrency industry as it nears sovereign recognition. The Blockchain protocol could be revised to limit transactions to KYC-verified wallets only. All transactions could be traced back to an identified e-wallet. Moreover, AML risk analysis and alert and report-generating mechanisms could be integrated within the crypto-system, instead of monitoring only the entry and exit points.

A “user” is a person that obtains virtual currency to purchase goods or services. A user of virtual currency is not an MSB under BSA and not subject to the regulation. Based on this definition if you purchase for reasons such as investing and not for the sole and express purpose of purchasing goods or services, you are neither an exchanger (not a business) nor a user (not purchasing goods or services). Instead, this purpose is undefined in the guidance, and the compliance obligations are unclear. There has been clarification that businesses who invest in cryptocurrency are users and not exchangers, but there was no clarification issued on personal investments.

An “administrator” is a person engaged as a business in issuing (putting into circulation) a virtual currency, and who has the authority to redeem (to withdraw from circulation) such virtual currency. Administrators only exist in the centralized virtual currency context because of decentralized virtual currencies like Bitcoin, once released, the units of cryptocurrency are out of the control of the developers and maintainers for the network. (Valkenburgh, 2017)

Conclusion

The regulatory landscape surrounding these cryptocurrencies is adapting slowly to the increasing demand. In parallel, Blockchain protocol may need to move quickly to offer KYC-verifiable wallets. On one hand, we see a lot of uncertainty from regulators around virtual currency, so it is justifiably still the Wild Wild West. On the other hand, it seems the benefits to certain existing regulations are clear and could be transformational, especially with regards to BSA requirements. So it’s important to pay attention and to be educated about regulatory requirements that might apply to individuals and businesses. The role of cryptocurrencies in our economy is just beginning. As time changes regulation will too, but like with most government driven agencies, regulation is slow to react and adapt. As consumers, we have a responsibility to make smart and informed decisions related to cryptocurrency.